Imagine a world where all money is digital. Instead of carrying coins and notes in their purse, people would keep digital currency units in electronic wallets on phones, watches or other electronic devices. Paying at the farmer’s market, giving the kids pocket money for lunch, settling the tab at a bar—all of this could happen digitally the way cash is handed over today: in real time, irreversibly, with no additional fees, using legal tender fully backed by the faith and credit of the national treasury.

Around the world, central banks from England to China have publicly floated the notion of issuing their own national digital currencies. Conceptually, they like the idea of harnessing the upside of the digital revolution—mobile payments, in particular—while preserving the existing legal and regulatory set up. Practically, they expect significantcost savings, a reduction of operational and fraud risks in the current payments systems, and a strengthened ability to execute monetary policy.

From a consumer’s perspective, the prospect of a digital British Pound Sterling or Renminbi is still mind-boggling. Which means, of course, societies would not go completely digital overnight. Instead, central banks could start issuing digital currency units alongside notes and coins as base money and adjust the mix over time, according to uptake. Once critical usage levels are reached and network effects kick in, universal adoption could happen very quickly.

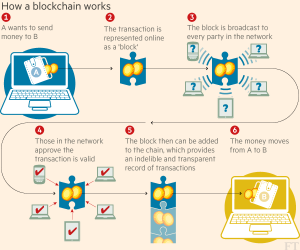

The key requirement for central banks to feel comfortable with issuing their own digital currency, and for consumers to embrace it, is ironclad integrity and security of the underlying technology. For a while, the best-known contender to provide an approach might have been Bitcoin and its underlying blockchain technology. Recently, however, specialists have alerted that the Bitcoin blockchain does not seem to be anywhere near industrial strength to support the vast transaction volumes required for a ubiquitous digital sovereign currency. Bitcoin settlements today only happen every 10 minutes—an eternity for frequent retail payment use throughout any given day. In addition, in the case of Bitcoin, the public-ledger technology is intrinsically linked to the concept of an alternative, private currency, because the so-called Bitcoin miners are compensated for their efforts to verify the veracity of a new block of transactions with new Bitcoins.

The key requirement for central banks to feel comfortable with issuing their own digital currency, and for consumers to embrace it, is ironclad integrity and security of the underlying technology. For a while, the best-known contender to provide an approach might have been Bitcoin and its underlying blockchain technology. Recently, however, specialists have alerted that the Bitcoin blockchain does not seem to be anywhere near industrial strength to support the vast transaction volumes required for a ubiquitous digital sovereign currency. Bitcoin settlements today only happen every 10 minutes—an eternity for frequent retail payment use throughout any given day. In addition, in the case of Bitcoin, the public-ledger technology is intrinsically linked to the concept of an alternative, private currency, because the so-called Bitcoin miners are compensated for their efforts to verify the veracity of a new block of transactions with new Bitcoins.

There are efforts to separate the block chain technology from the libertarian concept of a private currency that central banks are unlikely to embrace. Such efforts to trace the exchange of digital money via a public ledger could be combined with the counter intuitive concept of creating cryptographically protected digital currency units offline and injecting them into current payments systems, much like central banks distribute notes and coins to retail financial intermediaries today. At Omidyar Network, we have backed a solution that works in that way. More than a ledger, eCurrency Mint (eCM) provides an end-to-end solution that combines hardware, software, and cryptographic security protocols to enable a country’s central bank to not only issue digital sovereign currency, but also fully manage its operation, including the ability to monitor its movement through payments systems in near-real time.

In most emerging markets and developing countries, the current formal financial system only reaches a minority of the working-age adult population. Smallholder farmers, self-employed households, and micro-entrepreneurs have to rely on the age-old informal financial mechanisms such as rotating savings clubs, moneylenders, and pawnbrokers. These mechanisms can be unreliable and very expensive.

In most emerging markets and developing countries, the current formal financial system only reaches a minority of the working-age adult population. Smallholder farmers, self-employed households, and micro-entrepreneurs have to rely on the age-old informal financial mechanisms such as rotating savings clubs, moneylenders, and pawnbrokers. These mechanisms can be unreliable and very expensive.

For policymakers from the global south, the digitization of retail payment systems and financial services has become an important economic development priority. It offers the prospect of reaching far more people at far lower costs with the broader range of financial services they need to build resilience and capture opportunities. The 2015 annual gathering of some 300 central bankers and policymakers from 90 countries who have formed the Alliance for Financial Inclusion dedicated the bulk of the agenda to explore such innovations, which could deepen formal financial intermediation of their economies.

The idea of a central bank-issued digital currency might well be the type of “soft infrastructure” investment that brings direct and immediate efficiency gains. But perhaps more importantly, it would also accelerate and help scale a wave of service innovations that help advance financial inclusion, stimulate economic growth, and ultimately spur social progress.

The idea of a central bank-issued digital currency might well be the type of “soft infrastructure” investment that brings direct and immediate efficiency gains. But perhaps more importantly, it would also accelerate and help scale a wave of service innovations that help advance financial inclusion, stimulate economic growth, and ultimately spur social progress.

This article was culled from www.weforum.org

Recent Comments